The allure of high yields: what lies beneath

High yield credit funds often appear enticing, promising higher returns compared to traditional fixed income assets. But beneath the surface, they come with hidden complexities that can catch investors off guard. While these funds can generate strong income, risks such as liquidity constraints, market sensitivity, and potential defaults lurk in the background, waiting to surface during periods of economic stress.

Private credit: a double-edged sword

Private credit has become a go-to alternative as banks retreat from corporate lending across the world. But not all private credit opportunities are created equal. Investors must weigh key considerations, including:

Sector focus: Are the loans directed toward stable industries or volatile sectors like property development?

Business maturity: Are the borrowers established firms or distressed companies seeking last-resort financing?

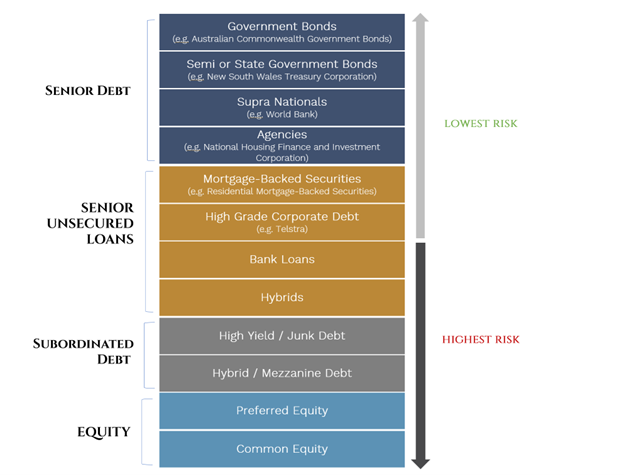

Capital structure positioning: Are loans secured with priority claims or unsecured with greater risk exposure? In other words, what is the order in which a lender gets paid back in the event of a company’s financial difficulties or liquidation.

Loan terms: Are the agreements structured to protect investors, or do they favour flexibility for borrowers?

While private credit offers a pathway to strong returns, failing to assess these variables can lead to unexpected risks that may only become apparent when markets take a turn.

Liquidity: the trap of limited access

One of the most overlooked risks in private markets is liquidity—or the lack of it. Unlike public market investments that can be easily traded, private credit funds often impose long lock-up periods and infrequent redemption windows. When market stress hits, liquidity can dry up quickly, leaving investors trapped.

The market dislocations of March 2020 highlighted that during times of market stress, fixed income funds may raise "sell spreads" to limit investor exits, making it more difficult to liquidate investments at desired prices. This exposed the illusion of liquidity, showing that what may appear to be easily tradable assets can become illiquid during periods of crisis. It serves as a reminder that investors need to carefully assess the true liquidity risks of their investments, particularly in volatile market conditions.

Default risk: the cost of chasing yield

The trade-off for higher returns is greater default risk. When companies face financial strain, meeting debt obligations becomes challenging, leading to potential losses for investors. The volatility of high yield credit means that economic downturns can cause sharp declines in asset values. Just as a seemingly stable structure can collapse under hidden weaknesses, a single borrower default can unravel expected returns, making portfolio risk management essential.

Transparency: seeing beyond the surface

Valuation discrepancies in private credit add another layer of risk. Unlike publicly traded securities, private credit valuations are periodic and can be slow to reflect market realities. Some funds may not fully account for borrower difficulties in their assessments, leading to overinflated valuations. This lack of transparency can obscure true risk levels, leaving investors with an incomplete picture of their exposure.

Property construction loans: a high-risk sector

Within private credit, property construction loans present additional uncertainties. These loans carry heightened risk due to potential project delays, cost overruns, and regulatory challenges. If a developer runs into trouble, repaying loans can become difficult, increasing default risk. Investors need to be particularly cautious, as construction loan liquidity is often low, making early exits difficult and potentially costly.

A stabilising force amid high yield credit volatility

To offset the unpredictability of high yield credit, government bonds can provide a stabilising force. While rising interest rates have made some existing bonds less attractive, new issuances offer higher yields, improving their appeal. As inflation moderates and rates decline, Australian government bonds are likely to benefit, offering stability and capital appreciation with expected rate cuts and price gains over the next 24 months. These assets serve as a crucial counterweight in diversified portfolios, helping to manage risk while ensuring a steady income stream.

Additionally, bonds rated AAA are considered to be of the highest quality and are associated with the lowest level of risk. They are often issued by governments with strong and stable economies, excellent credit histories, and a very low probability of defaulting on their debt obligations.

Top of the stack: What seniority means for bondholders

Striking the right balance

The key to navigating fixed income investing is striking the right balance. High yield credit funds can play a role in generating returns, but they should not dominate an investment portfolio. Instead, blending high yield opportunities with more stable assets—such as government bonds—can create a more resilient approach. Investors who focus solely on high returns without accounting for risk may find themselves exposed to hidden dangers when markets shift.

By understanding the underlying risks and ensuring diversification, investors can build a portfolio that maximises opportunity while safeguarding against unforeseen challenges. In today’s dynamic market, getting the balance right is the key to long term success.

Learn more about Jamieson Coote Bonds

For more information on Jamieson Coote Bonds and their funds and strategies visit their website.