Managing change in a managed accounts transition

Making a successful transition to managed accounts: change management considerations

Completing a successful transition to managed accounts can be a difficult and at times, quite confronting experience. The transition journey isn’t as simple as the traditional experience of moving from Investment Manager A to Investment Manager B. It can involve a far more involved process; including a change of advice model, a possible introduction of non-traditional asset managers and often a need to switch technology partners and ultimately the client engagement experience. The benefits to both your business and your clients in making the transition can, however, be truly transformational. With increased business efficiency and more time to spend with clients and on your business, practices can benefit from enhanced levels of client satisfaction, improved retention and increased profitability that can drive success long into the future.

There are three key stakeholders in delivering this change; the adviser, the client, and the practice support staff. Ensuring all stakeholders’ needs are considered and that all parties are aligned is important to both the success of the transition and in building trust between the stakeholders. Without it, unforeseen barriers and complications can severely hamper the transition.

Change management will play a pivotal role in whether or not the move to managed accounts is a seamless and successful experience. It will determine the extent to which practice principles embrace the opportunity to future proof their business and subsequently increase profit and eventually enhance their business valuation. Praemium’s Managed Accounts research (conducted by Business Health) points to an increase of 85% in profit, where a practice has embraced a managed account solution for more than 75% of their clients, compared to practices that have not yet embarked on this journey. Therefore, there is a significant incentive in not only making a successful transition but also applying it to the widest number of client segments in your business as possible.

Before embarking on this strategic decision it is worth taking some time to consider what change management means and how it could impact success.

Change Management in the context of Managed Accounts

For successful business owners, change management is a core capability, focused on engaging people within an organisation to adapt to new processes, possibly accepting new behaviours, and ultimately building a sustainable outcome. However, it is not just a change in internal discipline. Business owners must consider their clients as a key stakeholder in the transition and build in plans to ensure clients adjust their expectations of the service delivery model, regardless of whether the change would be deemed to be positive.

The following 6 considerations of Change Management can help smooth the transition to a new business model.

Consideration 1: Define and detail your business model

Taking the time to define and detail your business model will ensure that you have a framework to develop a strategy and make enduring and sustainable decisions for your business. Too often short-term tactical decisions, that are not linked to an overall strategy, are made by SMEs which then become more of a hindrance than a catalyst for success.

Many industries within the SME sector are grappling with the speed in which their client’s needs are changing, providing relevant services to a changing demographic and using technology at a scale relevant to their business. Research from Ricoh, a workplace technology specialist, shows that only 40% of Australian organisations have a detailed enough level of clarity around required systems and processes, indicating the challenges many businesses will face in keeping up with the pace of change.

Without a clearly defined business model, the ability to develop the requisite strategic plan and operational roadmap to keep pace with this changing environment is intuitively challenged. It also makes it difficult to define how or why managed accounts can help achieve your business goals and what is required to successfully roll out the concept to employees and clients.

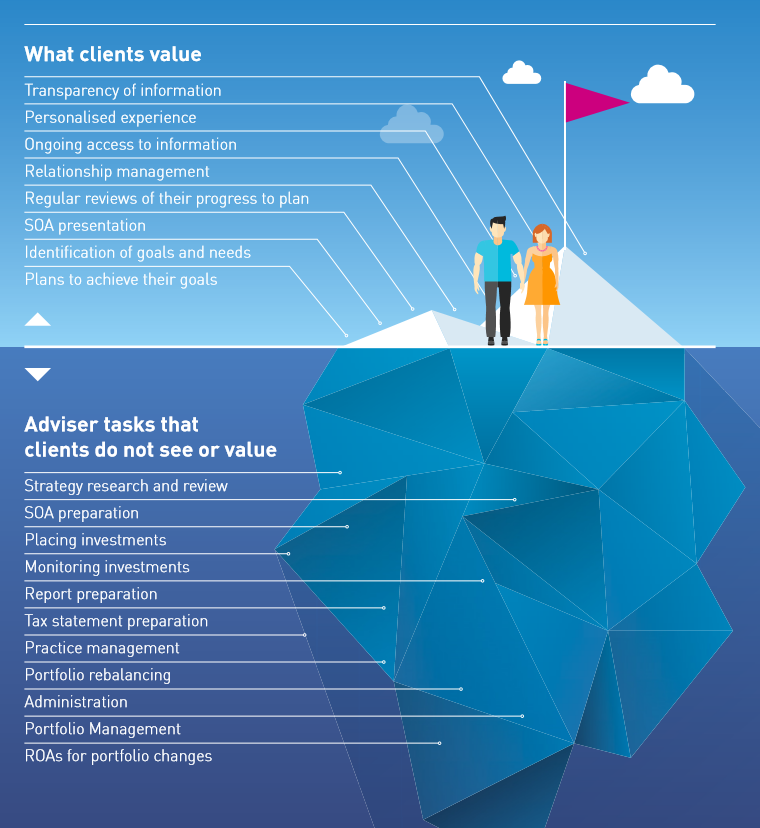

Consideration 2: Understand Your Customer

Peter Drucker, a management consultant whose work contributed to the foundations of modern business, asked the question ‘Who is the customer and what do they value? A good business model blends these questions with, ‘How do we deliver value that can then generate revenue and ultimately increase profit?

Financial Services has a constantly changing regulatory and legislative landscape. As a result, practice principals may be forced to adjust processes or business models to directly address a legislative change. Most customers, however, have little interest in these issues and are naturally more concerned with the value they are receiving from the advice process.

Many SMEs will design a business model around their own goals or set of beliefs and then search for clients to generate revenue. Successful business models, however, are built around solving specific client problems or delivering on specific client needs.

Understanding what your client’s value, and do not value, will determine your level of success.

Clients are a key stakeholder in your business and fundamental to its success. There is a growing preference amongst investors for a digital service, with 40% of customers preferring self-service over human contact (Aspect) and 50% believing their adviser should have a digital solution (Accenture). It is imperative that business owners understand how these needs impact the effectiveness of their client engagement model and how choosing the right technology provider can help them deliver a service their clients find relevant and valuable. A successful transition to managed accounts will need to address client’s needs now and into the future.

Consideration 3: Create a change management plan

With any project having a clear understanding of your goals and the ability to clearly articulate what you are trying to achieve, will make it much easier to develop a robust plan.

Writing down any significant change in your business and defining your business model will help you plan accordingly and communicate your approach to staff and clients alike. It will enable you to gain buy-in from your team upfront, as they will be integral to the success of the new approach. As you may require employees to embark on new skills or knowledge training, you will want them engaged and involved in helping to identify the impact on other processes and procedures within your business. Importantly they are often client-facing and need to be able to articulate the same message to ensure a consistent client experience.

When documenting your plan, you should consider:

» What will your business look like post the change?

» What are you aiming to achieve?

» Why are you doing this and how will it support your Investment and Advice Model?

» What are the benefits to all stakeholders?

» What are your technology needs and what is the universe of providers to review?

» What tasks through the process will need to be done and who will be assigned the responsibility?

» Key milestones to hit as you progress through the project

» What are the measurable goals once the project is finished?

A simple way to structure your plan is to break it down into stages. Imagine a series of gates and to open each gate you need a certain amount of information or to have achieved certain milestones before the gate will open. Between each “gate” clearly define what needs to be achieved and by whom. By defining these stages, you can also set target completion dates and create a timeline for your project. This will ensure everyone knows their role, what they are assigned to deliver and in what timeframe. If a timeline assigned to a particular stage is not achieved, then the timeline can be adjusted for subsequent stages and a new overall timeline can be easily set.

Consideration 4: Engage your clients early

As your business embraces change it is advisable to bring your clients on the journey as early as possible. Financial planning at its core is a technical skill, running a business requires practical skills and building a client base requires soft skills. Change management, which has a major impact on the way you give and subsequently deliver advice through your engagement model, will place greater emphasis on your soft skills through the process.

This will be easier if, as part of your planning process, you have delivered on the first three considerations; defining your business model, understand your customer and create a defined plan. These will give you the foundation to clearly articulate the changes and benefits to your clients and allay any of their own change management fears. If your managed accounts journey is limited to reducing your RoA burden, you may find that your clients see the change more cynically, as a change that benefits you rather than them.

There are many ways to bring your clients on your journey and how you choose to do this will need to take into account your own business and client base. Some ideas you could consider are;

Educate early – Communicate to your clients, as early as possible, that you are looking at managed accounts on their behalf. Consider educational newsletters or even webinars to explain what you are researching and why. Utilise surveys to gain any early concerns or feedback and consider client information sessions, where appropriate, to speak directly to your clients about your strategy.

Focus Groups and Beta Testing - Bring small groups together of different client segments, either virtually or physically, to discuss the strategy, changes, and benefits etc. Consider how you will introduce your strategy; how you will articulate the changes and importantly have defined a very clear engagement model and set of benefits you can present. Before you embark on a full roll-out consider beta testing a few different client types, particularly if you are embracing new technology partners. Map the approach, engage staff and clients to provide feedback on each stage of the process and only consider a mass roll-out once you have ironed out any factors that are causing friction to your client engagement experience.

Ongoing Communication – As you work through your change of advice model, provide regular and clear updates to your wider client base. This will ensure clients are coming on the journey with you but importantly it will increase their trust in what you are trying to achieve and ensure they are engaged and informed when you finally sit down to implement it with them.

By addressing this successfully you will be able to deliver on the practical aspects of implementing managed accounts in your business and also make client onboarding a seamless and time-efficient experience.

Consideration 5: Engage Your Team

Engaging teams in special projects offer real benefits to a business. In their Global Culture Report, O.C. Tanner found that employees who are involved in special projects have a 20% increase in job satisfaction and 75% of those surveyed felt special projects helped them develop skills that their day to day role would not.

Transitioning to managed accounts is a major event for a planning practice and engaging and empowering the whole team to be involved will increase employee satisfaction and help to ensure that you have undertaken a robust fact-finding exercise that will assist the business in areas such as:

- Identifying current or future barriers

- Determining which processes will need to be addressed and amended, minimising future administration problems

- Providing a greater understanding of needs when choosing new partners such as technology and investment partners

- Increase clarity across the business and reduce time to roll-out the strategy.

The team's ongoing involvement in the project will also lead to a more efficient rollout. A clearly defined plan with assigned tasks and responsibilities will provide a greater level of focus and significantly reduce the delivery time.

As mentioned, a significant benefit of engaged and informed employees is that the messaging to clients is consistent and positive. The worst outcome would be confused clients and disconnected employees limiting the success of such an important change.

Consideration 6: Manage the project slowly and expect setbacks

Very few projects or change management events run smoothly and exactly to plan. The business needs to be adaptable to change and ready for setbacks, which should be treated as hurdles rather than roadblocks. This often comes down to strong leadership and the culture of the business allowing for mistakes without recrimination of 20/20 hindsight.

However, following a considered change management plan will ensure the setbacks can be minimised. By understanding what you need to achieve and for whom, map the project through manageable stages, utilise all IP and resource in the business and understand and engage with your clients through the journey you can deliver a great outcome for all stakeholders. The potential rewards for your practice in transitioning to managed accounts will make the work involved more than worthwhile.